Republic of the Congo

Overview of timber sector of the Republic of the Congo

Supply chain actors

There is a total of 60 forest concessions, which are allocated to 35 forestry companies.

The 3 major companies in terms of allocated spaces are CIB (>2M ha), IFO and SEFYD (>1M ha each).

Production and processing

Main harvested species

Although over 50 species are harvested, two-thirds of the logs are of only two species:

- Okoumé (Aucoumeaklaineana)

- Sapelli (Entandrophragmacylindricum).

Okoumé is harvested in the southern forest massif and Sapelli in the northern forest massif.

Other frequently harvested commercial species include (FRMi 2018):

- Ayous (Triplochitonscleroxylon)

- Bossé (Guareacedrata)

- Iroko (Miliciaexcelsa)

- Kossipo (Entandrophragmacandollei)

- Limba (Terminaliasuperba)

- Padouk (Pterocarpus soyauxii)

- Sipo (Entandrophragma utile)

- Wengé (Millettialaurentii)

- Tali (Herythrophleumivorense)

- Okan (Cylicodiscusgabunensis)

- Mukulungu (Autranellacongolensis)

The northern forest massif, which is much larger and the richest in terms of high-value species, only really started to be harvested as of 1970. Almost all of these forests are now covered by logging operations. Today, most output comes from the northern zone covered by larger forest concessions.

Despite the strategic importance accorded to the development of the industrialisation of the timber sector by the Congolese government, the industrial infrastructure is not yet sufficiently developed to achieve the objective of halting the export of logs set out in Law 33-2020 of the forestry code and in a recent (2020) CEMAC decision. The dominant activities still relate to primary processing, namely sawing, peeling and the manufacture of plywood.

There are currently 61 timber processing units of all types, and some companies have made significant investments to support the strategy of extensive and diversified local timber processing.

Most timber processing units in the southern forestry sector are old and not very efficient, compared to the industrial units located in the north of the country. Artisanal woodworking remains informal and of low quality due to the poor quality of the raw material that is used (wet sawn timber).

The official production in forest concessions represents 83% of the country's total production, compared with 17% for the non-official sector outside forest concessions.

The local timber market is still highly undersupplied in terms of processed products from forestry concessions. In 2018, the volume of sliced logs put on the local market reached approximately 19,257 m3.

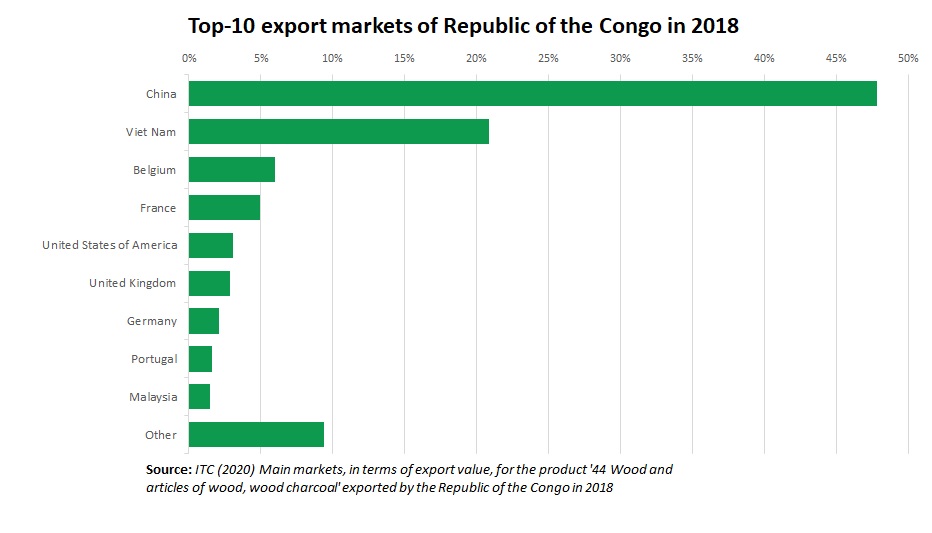

Export

According to the MEF, total forest production in 2018 was around 1.8 million m3 of which 44% (0.8 m3) was exported as logs. Over 80% of output was exported to Asia, 16% to Europe and under 1% to Africa. The remainder of Congo's timber production is exported as sawn timber.

The Congolese timber industry therefore remains partly focused on the export of logs, despite the legal obligation (since Law 16-2000) to transform a minimum of 85% of the logs produced by each forestry company operating on Congolese territory. Recently, new measures have been taken by the Congolese government to increase the rate of log processing: the new forestry law (Law 33-2020) provides for the full processing of logs on national territory, with the exception of a list of species that has yet to be defined. Nevertheless, the strategy remains the strict prohibition of log exports by 2022, as provided for by the CEMAC. Other incentives are also being considered to increase log processing levels, including fiscal measures.

Logistics infrastructure

Northern Congo is relatively landlocked and far from shipping ports.

The main export route for timber and timber products is via the Pointe-Noire port in the south of the country, and the Douala port in neighbouring Cameroon.

Data table

| Production (X 1000m3) |

Imports (X 1000m3) |

Domestic consumption (X 1000m3) |

Exports (X 1000m3) |

|

|---|---|---|---|---|

| logs | 2.193 | 0 | 1.253 | 941 |

| Sawnwood | 332 | 1 | 160 | 173 |

| Veneer | 47 | 0 | 32 | 14 |

| Plywood | 30 | 0 | 30 | 0 |

ITTO (2019), data 2017