Philippines

Overview of timber sector of Philippines

Supply chain actors

Timber is either imported from international market or sourced locally through tree growers or log traders. The typical national timber supply chain starts with the establishment of a tree plantation by a tree farmer or grower (see Section 1.2 and 1.3 for tenure instruments who are allowed to grow timber). Trees are harvested and transported to wood processing plants by 141 mini sawmills, 52 veneer plants, 13 plywood plants, 15 regular sawmill, 8 integrated plants, 4 blockboard plants (PFAG, 2020), paper and pulp millers, furniture makers, and other downstream actors. Products produced from processing are sold to consumers or end-users.

Imported products (2019) and the corresponding top trading partners for each product are (1) paper and articles of paper and paperboard – China, Indonesia, Japan, (2) forest-based furniture – China, Malaysia, Japan, (3) pulp and waste paper – USA, New Zealand, Thailand, (4) other wood-based manufactured articles – China, Japan, Vietnam, and (5) lumber – Canada, Ukraine, Finland (FMB, 2019; PFAG, 2020).

Production and processing

Main harvested species

Species harvested as round logs in order of importance (m3/year) (FMB, 2019):

- Falcata (Paraserianthes falcataria) - 632,574 m3

- Mangium (Acacia mangium) - 118,758 m3

- Mahogany (Swietenia macrophyllla) - 76,891 m3

- Yemane (Gmelina arborea) - 62,279 m3

- Bagras (Eucalyptus deglupta) - 16,354 m3

- Para Rubber (Hevea brasiliensis) - 11,928 m3

- Rain tree (Albizia saman) - 3,436 m3

- Ipil-ipil (Leucaena leucocephala) - 2,507 m3

- Others (23,376 m3) which may include:

- Kakawate (Gliricidia sepium)

- Marang (Artocarpus odoratissimus)

- Mango (Mangifera indica)

- Durian (Durio zibethinus)

- Auri (Acacia auriculiformis)

- Red Gum (Eucalyptus camaldulensis)

Primary wood processing plants produce veneer, plywood, fibreboard, and lumber from high grade logs. The primary wood products and some low-grade logs are processed by secondary wood processing plants or sold to the international and domestic market.

Secondary wood processing plants include furniture makers, construction material makers, wood packagers (wooden containers), and other wood-based makers.

Export

The export value of timber products in 2019 is limited only with a total amount value of USD 631.81 M FOB constituting lumber (28.9%), pulp and waste paper (22.2%), paper and articles of paper and paper board (19.7%), forest-based furniture (11.6%) and other wood-based manufactured articles (10.2%). In 2019, only fuelwood was exported as roundwood with a total volume of 5,021 m3 (USD 249,250). Processed wood products such as lumber and veneer are also sourced by the international market, having 89 (USD 177,295) and 15 (USD 11,148) thousand m3 exported in 2019, respectively (FMB, 2019).

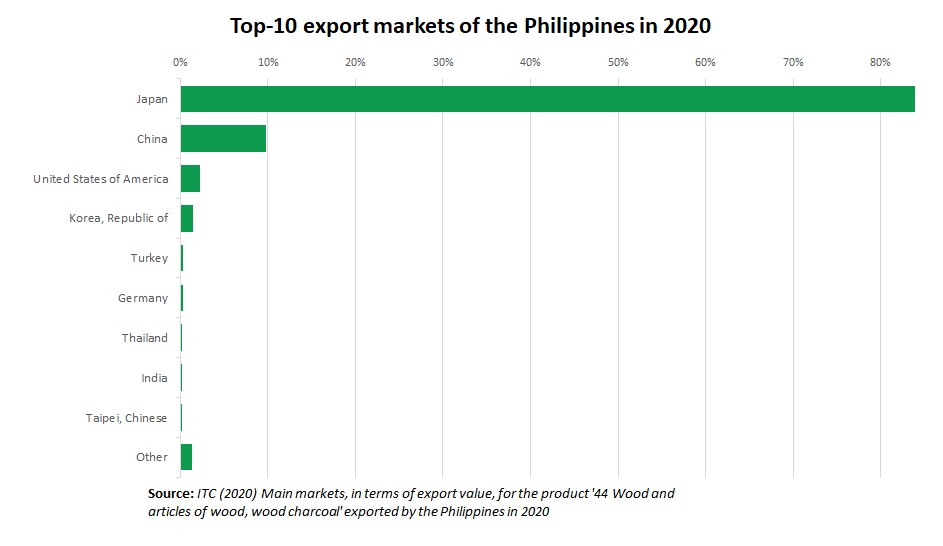

Exported products and destinations (2019) for each product are (1) lumber – Japan, USA, China, (2) pulp and waste paper – UK, Netherlands, Japan, (3) paper and articles of paper and paperboard – USA, Indonesia, Taiwan (4) forest-based furniture – USA, Japan, Netherlands, and (5) other wood-based manufacture articles – Japan, USA, South Korea (FMB, 2019; PFAG, 2020).

Logistics infrastructure

The following are the designated timber import and export ports (DTI, 2018):

- Luzon –Sta Ana, Cagayan; Subic Bay Port; South Harbor Manila; North Harbor Manila; Batangas City Port

- Visayas – Cebu City;

Mindanao – Cagayan De Oro City; Butuan City;; Davao City; Zamboanga City; General Santos City.

Data table

| Production (X 1000m3) |

Imports (X 1000m3) |

Domestic consumption (X 1000m3) |

Exports (X 1000m3) |

|

|---|---|---|---|---|

| logs | 3.928 | 14 | 3.942 | 0 |

| Sawnwood | 246 | 543 | 464 | 325 |

| Veneer | 61 | 102 | 163 | 0 |

| Plywood | 210 | 847 | 1.047 | 10 |

ITTO (2019), data 2017